A PFIC is a U.S. tax classification applied to certain non-U.S. investment funds/companies that earn most passive income. To understand this we need to under the key difference between active and passive income.

Active Income – You perform work to earn income. For example, running a business or working a job.

Passive Income – Your money generates income for you. For example, if you have excess capital, you can invest it and earn interest, dividends, rent, or capital gains.

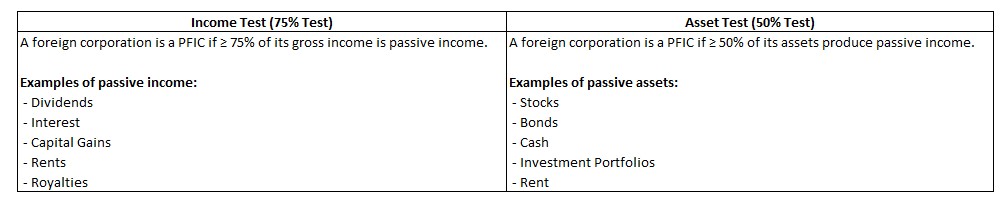

When does a foreign company or fund become PFIC? When either of the following test is true –

The key point to remember that for PFIC it is the company’s income which matters and not the US tax residents income. For e.g., PFIC applies when a US tax resident invests in a foreign corporation whose income or assets are primarily passive. Mutual funds are structured as corporations and earn passive income, so they meet PFIC criteria.

For example:

- If XYZ Ltd is a manufacturing company based in London, it earns active business income from producing and selling goods. Because its income is active, XYZ Ltd is NOT a PFIC, even if a US tax resident receives dividends from it.

- But if a US tax resident invests in a UK‑domiciled mutual fund, the fund itself earns passive income (dividends, interest, capital gains) from holding stocks and bonds. Because the fund’s income is passive, the mutual fund IS a PFIC, regardless of what companies it invests in.