Sharpe and Sortino are risk ratios.

Sharpe Ratio:-

Sharpe ratio indicates the investor about how much of the risk is converted into return. Think of it like this: “If I take one unit of risk, how much reward am I getting above the risk free rate?”

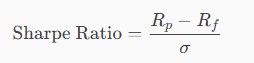

Formula –

Where:

Rp = Portfolio Return (Our chosen investment e.g., mutual fund)

Rf = Risk free rate (e.g., Bank of England (BoE) rate)

![]() = Standard Deviation of portfolio return (i.e., total risk)

= Standard Deviation of portfolio return (i.e., total risk)

Understanding the formula and the logic –

Rp – Rf = Risk premium. Say, BoE rate is 3%.Investing into a government bond (Gilt in the UK) is always safe. Instead of investing into a gilt we decide to invest into a mutual fund which is risker than the gilt. Since, we take extra risk we expect some extra return too. Therefore, the excess return which the mutual fund gives in comparison to investing in gilt is known as the risk premium.

Why is this important for Sharpe Ratio?

The Sharpe ratio uses risk premium (as explained above) in the numerator because it focuses on reward above the safe baseline. Then it divides by standard deviation (total risk) to get to the ratio of risk premium to total risk.

Why Standard Deviation (SD)?

SD is a number that tells you how bumpy the ride is.

High SD = wild swings (more risk)

Low SD = smoother ride (less risk)

So, SD is like measuring how uncertain or unpredictable the fund is.

Why divide by SD in Sharpe ratio?

Let’s say you earn extra return above the risk free rate – that’s your reward (Risk premium – as explained above)

But if your fund is very volatile, that reward is less impressive, because you had to endure a bumpy ride to get it. So we divide by SD to ask:

“How much reward did I get for each unit of bumpiness?”

Therefore, Sharpe ratio is

in other words:

How much risk premium did you earn for each unit of total risk you took?

The higher the better. A higher Sharpe ratio is always better as it says that the extra risk you took is well compensated with the excess return over the base rate.

Sortino Ratio:-

Sharpe Ratio uses total SD i.e., both upside and downside swings (risk).

If your fund jumps up a lot (big gains) or down a lot (big losses), Sharpe counts both as risk

But is up side risk really bad? Not necessarily.

Instead what Sortino Ratio says:

“Let’s only count the bad bumps – the downside risk.”

It ignores positive swings because investors usually don’t mind making more money than expected.

What does downside deviation mean?

It measures how much returns fall below a minimum acceptable level (often 0% or the risk-free rate).

If your fund rarely dips below that level, downside deviation is low → Sortino Ratio looks good.

If your fund crashes often, downside deviation is high → Sortino Ratio looks bad

A higher Sortino Ratio is better because:

It means the fund (or any other investment) rarely dips below the minimum acceptable level (often risk free rate).

Downside deviation is low, so the denominator is small.

Therefore, the ratio is larger, showing the fund delivers good returns with minimal bad volatility.

Formula of Sortino Ratio –

The Sortino Ratio measures risk-adjusted return, but it focuses only on downside risk, unlike Sharpe Ratio which uses total SD.

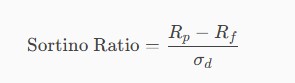

Formula –

Where:

Rp = Portfolio Return (Our chosen investment e.g., mutual fund)

Rf = Risk free rate (e.g., Bank of England (BoE) rate)

![]() = Downside deviation (SD of negative returns or returns below a minimum acceptable threshold)

= Downside deviation (SD of negative returns or returns below a minimum acceptable threshold)

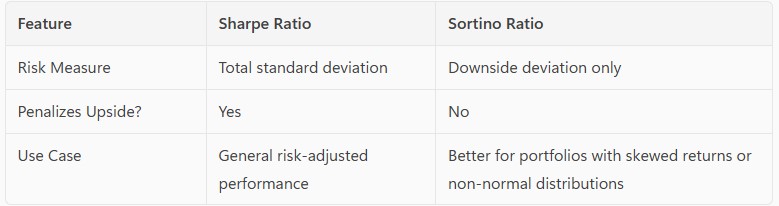

Key Differences between Sharpe and Sortino Ratios –

What does Penalise Upside mean?

Sharpe Ratio treats all volatility as risk – both upside (big gains) and downside (losses).

So, if the fund has wild positive swings, Sharpe still counts that as “risk”.

Sortino Ratio ignores upside volatility.

It only cares about bad volatility (returns below a threshold).

So big positive jumps don’t hurt your score.

Example of Each use case

Sharpe Ratio use Case

- Comparing two diversified mutual funds or ETFs.

- Example:

- Fund A: 8% return, SD = 10%, Sharpe = 0.5

- Fund B: 6% return, SD = 4%, Sharpe = 0.75

- Even though Fund A has higher return, Fund B is more efficient per unit of total risk.

Sortino Ratio Use Case

- Evaluating a hedge fund or strategy with skewed returns.

- Example:

- A fund that sells options might have lots of small gains and occasional big losses.

- Sharpe Ratio penalizes the small gains (upside volatility).

- Sortino Ratio focuses only on the big losses, giving a clearer picture of downside risk.